How to improve your financial wellbeing for retirement

Securing your financial wellbeing is always important, but especially in later life. Find out how to improve your financial wellbeing for retirement in our guide.

Why improving your financial wellbeing in retirement matters, and how to do it

When you hear the word ‘wellbeing’, you might think of your health. Being ‘well’ usually means being healthy, both physically and mentally.

But there’s more to wellbeing than your physical and mental health. Financial wellbeing is just as important and it can be closely linked to your overall health, as they can all affect each other.

Discover what financial wellbeing is, why it’s particularly important as you transition into later life, and how you can improve yours for retirement.

{{main-cta}}

What is financial wellbeing?

Financial wellbeing is the sense of security and freedom your wealth gives you.

To have financial wellbeing, you need to be secure and in control of your money. You must be completely able to meet your needs, and withstand unexpected shocks without them disrupting your life.

Financial wellbeing is closely related to good mental health. When you feel secure and confident with your money, your mental health is more likely to be good.

Meanwhile, poor financial wellbeing is linked to feelings of anxiety and depression. This can become a vicious cycle, with those with poor mental health making worse financial decisions, leading to poorer financial wellbeing, and so on.

Your mental and physical health can also affect one another. So, financial wellbeing can ultimately have an effect on both.

You can see why maintaining financial wellbeing is so important, both for your health and your wealth.

Why financial security is important for retirement

Underpinning financial wellbeing is financial security, which is crucial for a happy retirement.

Financial security is the knowledge that you have (and will continue to have) enough money to live.

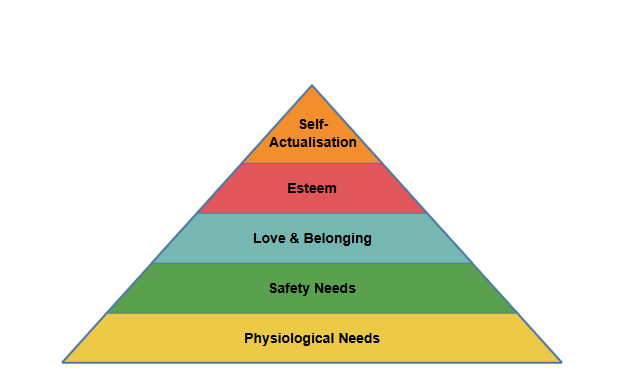

Think about Maslow’s hierarchy of needs. Displayed as a pyramid of layers, this famous theory shows what humans require to live. To reach the next stage, you have to fulfil the needs in the block below, building towards the top.

At the very bottom are our ‘physiological needs’. These comprise things such as food, water, shelter, and clothing. You’ll notice that money is vital for meeting even our most basic needs.

The next rung is ‘safety needs’, where financial security and safety nets sit. Knowing that you have the money you need to live and a safety net in case of an emergency is key for feeling secure.

Only once you’ve met these needs can you progress to those at the top of the hierarchy. These include love and belonging, esteem, and self-actualisation (that is, realising your full potential).

That’s why retirement and financial wellbeing are so closely intertwined. To enjoy your life, spend time with loved ones, and realise your full potential, you need financial security. In turn, that’s what creates financial wellbeing.

Financial considerations when planning for retirement

Financial wellbeing and security are both important, throughout your career and in retirement. However, the playing field changes in later life.

You’ll likely have a different range of financial concerns in retirement. Here are a few to consider.

Your goals and what you want to achieve

Ending your working life and retiring can feel like an end. But it’s actually a transition into a new life stage where your goals and ambitions change.

Your goals will be personal to you. But some common retirement targets include:

- travel;

- learning a new skill or pursuing a hobby;

- volunteering; or

- exploring a new career or even starting a business.

What you can achieve in retirement will depend on your finances and how much you’ve saved. So, think about your ambitions when planning for retirement.

Supporting your dependants

Another common target for many people is financially supporting their dependants. In particular, this includes children and grandchildren. You may want to help your loved ones with their own financial goals, such as going to university or buying a home.

Your spouse or partner could also be a dependant, especially if you’ve saved more for retirement than them. Think about how you've organised your savings so that you’re able to support your life together.

Mortgages and debts

Debt can be a useful tool, as long as it’s well-managed and you aren’t paying excessive interest on it. You may well have a mortgage or other personal loans that are easy to keep on top of during your career.

But in retirement, you’ll likely be drawing on your pensions and savings. These sources can run out if you’re not careful, and paying off mortgages and debts can put pressure on them.

Think about clearing debts, especially high-interest loans on credit cards or similar, before you retire.

Your other larger outgoings

It’s also worth considering other big outgoings outside of your usual spending. Think things like cars, holidays, and home renovations.

These might be manageable when you’re earning. But, they can also put pressure on your pension. Keep these in mind with your whole retirement budget.

How to improve financial wellbeing ahead of retirement

Whether you’re at retirement now, or still a few years away, it’s never too soon to start planning for later life. That includes thinking about how you can ensure your financial wellbeing and security.

Here are a few things you can do to potentially improve your financial wellbeing ahead of giving up work:

- Plan ahead - think about when you want to retire, anything you want to achieve, and your desired lifestyle. From there, you can create a budget and see what you’ll need to achieve it.

- Keep unexpected costs in mind - just as it’s suggested to keep an emergency fund during your working life, doing the same in retirement can be sensible. You might face unexpected costs that mean you need quick access to cash. Or a period of market volatility could temporarily reduce your pension’s value and make it more expensive to withdraw from your fund (accessible from 55, rising to 57 in 2028). Keep these costs in mind and consider maintaining that emergency fund.

- Clear mortgages and other debts as far as possible - as mentioned above, mortgages and other debts can quickly eat into your pension savings. So, looking to clear these before retirement can be sensible so you can use your pension and savings to enjoy life, rather than paying off debt. If your mortgage is set to last beyond your ideal retirement age, you could consider downsizing to free up the value within your home.

- Don’t forget about long-term care - as you get older and approach the end of your life, your likelihood of needing care increases. Whether that’s at home or in a facility, care can be very expensive. It’s worth thinking about the cost of this and possibly setting funds aside to pay for it. Otherwise, that burden could pass to your loved ones.

Plan for retirement the right way

There’s plenty to think about when planning for retirement. Financial wellbeing is one area not to overlook.

With that in mind, it’s worth thinking about how you’re managing your retirement savings, especially your pension.

No matter where you are in your retirement planning, make sure you’re putting enough into your fund. That way, you give yourself the best chance of achieving your later-life goals. Even small increases in what you’re contributing can make a big difference.

It can also be helpful to consolidate your pensions. You might have more than one pension, especially if you’ve worked for many employers and were auto-enrolled into their schemes.

Consolidating them can make it simpler to manage your savings and see how much you have, all in one place.

It’s straightforward to combine your pensions with PensionBee. You can put your eligible pensions into a single pot, and view your retirement savings easily via the website or PensionBee app.

As long as it’s right for you, consolidating your pensions could help you on your way to achieving financial wellbeing, both now and in retirement.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Last edited: 05-03-2026

Be pension confident!

Be pension Confident!

- Sign up in minutes

- Transfer your old pensions into one new online plan

- Invest with one of the world’s largest money managers

- Pay just one simple annual fee