This article was last updated on 12/08/2025

As you enter your 50s, retirement may no longer be such a distant idea. Potentially, just a few years, rather than decades away, investing for retirement may be best served by a shift in approach.

When you’re further away from retirement, investments with a higher-risk/higher-reward can serve you better in the long term. They typically offer greater opportunities to grow and recover from market downturns. Our Global Leaders Plan is designed with that approach in mind. It’s aimed at savers further away from retirement to maximise their pension’s growth opportunity.

However, if you’re looking to start taking your pension as retirement income in the short term, you may want to consider a pension investment strategy that focuses on:

- preserving the money you’ve already built;

- steadier growth; and

- actively reducing the impact of market volatility.

PensionBee’s 4Plus Plan

Our 4Plus Plan aims to reduce the impact of market volatility compared to equities (company shares. It aims to protect balances and target growth, smoothing returns and bringing more certainty in the retirement years. It could be most suitable for people considering accessing their pensions in the near-to-medium term. This can support pension savers to transition more confidently into retirement while optimising their hard-earned savings.

Key features of the 4Plus Plan

Targeted growth

The 4Plus Plan aims to grow your savings by 4% per year above The Bank of England’s base rate over a recommended five-year period. It’s designed to grow the fund’s value above inflation so savers can withdraw a sustainable long-term income. This approach is also known as a target return strategy.

Risk management

The 4Plus Plan is actively managed. A team of money managers monitors global trends and adjusts how the plan invests on a weekly basis. This is a particularly important feature during periods of market volatility for those making withdrawals, as it can help to preserve retirement pots and protect against sequencing risk. Sequencing risk refers to the risk of making pension withdrawals when the market is down, which can have a negative impact on the long-term value of your retirement savings.

The 4Plus Plan’s long-term return target objective aligns with the 4% rule, the generally accepted rate for sustainable withdrawals, supplemented by modelling. This approach brings more certainty to those who wish to preserve their retirement pots whilst also making withdrawals, in a time of increased global instability.

4Plus Plan performance

Active management can play a crucial role during periods of volatility for those approaching or in retirement. It can soften the negative effects of falling markets on investments like pensions.

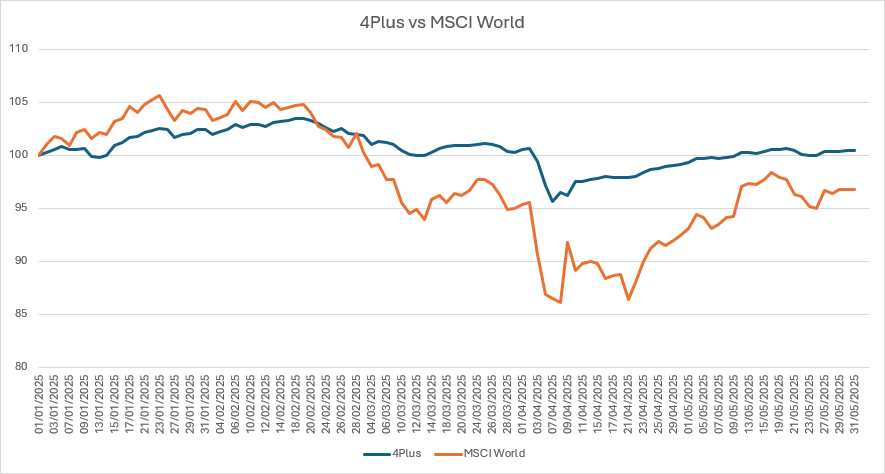

The following chart shows the 4Plus Plan’s performance (represented by the blue line) against MSCI World (the orange line) between 1 January and 31 May 2025*. MSCI World is an index that tracks the performance of the biggest public companies across developed markets. These include companies such as Microsoft Corp, Apple, and Tesla. It’s used here to show the performance of the 4Plus Plan compared to major global stock markets.

*with prices rebased to 100.

As you can see, the 4Plus Plan’s year-to-date performance is aligned with MSCI World when market volatility was low. However, it outperformed it between the end of February and the end of April. This is due to changes made by the 4Plus Plan’s portfolio managers to manage volatility as global equities (company shares) lost their value.

Early April is especially notable as a time of intense market volatility. This was driven, in large part, by the US President’s ‘Liberation Day’ announcement and subsequent tariffs on goods being imported into the United States. This news resulted in big market swings, which impacted the performance and value of many investments, including pensions. You can read more about what drove volatility in this period on our pensions and tariffs blog.

How the 4Plus Plan’s performed during historic market events

Since the plan’s inception in 2013, there have been multiple periods of volatility. Below you’ll find a list of a few recent and notable market events, as well as the above-mentioned US government announcements around tariffs.

Like many funds, the 4Plus Plan was impacted during these periods. However, as the table shows, the 4Plus Plan saw notably less decline in value compared to the FTSE World Index (which tracks global stock performance of both developed and emerging markets) in every case. The figures below represent how much in value a fund fell from its highest to lowest point before it started to recover.

During these periods, the plan’s money manager, State Street, responded to the particular market conditions at that moment. They did this by moving geographies and asset classes, such as:

- developed to emerging markets; or

- equities to bonds, real estate or cash.

This demonstrates the 4Plus Plan’s effectiveness in helping preserve the pension savings built up, as it reduces the impact of market volatility.

4Plus Plan performance during key market events

*Source: State Street, Investment Solutions Group. As of April 2025. Past performance is not a reliable indicator of future performance.

Summary

The 4Plus Plan’s active management gives it greater flexibility to respond to short-term market volatility. This approach serves the plan’s objective of helping those starting to think about drawing an income from their pension. It does this by adapting its approach to preserve the value of pension savings already built up in it.

This is why we’ve made the 4Plus Plan our default plan for customers aged 50 or over. For many people, at this point in their life, retirement considerations become more prominent. The 4Plus Plan can support you in preparing to make that transition.

Read about how our 4Plus Plan works in more detail on our dedicated blog.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |