This article was last updated 30/04/2025

Pensions have experienced some ups and downs lately, with balances rising and falling on a daily basis. The main driver of these changes has been fast-moving news around President Trump, tariffs and trade, and knock-on implications for inflation, interest rates and the economy. Here’s a recap of what’s happened this month:

- 2 April - President Trump begins introducing a number of tariffs (taxes on imported goods) on almost all countries, including key US trading partners like Canada, Mexico, China and the UK. This caused global stock markets to experience a sharp downturn.

- 9 April - a 90-day pause is announced with tariffs for most countries reduced to a baseline 1_personal_allowance_rate - other than for China, where a rate of up to 1_additional_rate remains on Chinese-made goods.

- 10 April - stock markets respond positively to the tariff pause announcement.

- 12 April - China responds with a 1_corporation_tax tariff on US goods, but says that it’ll not respond to any further US increases.

- 21 April - countries including Japan and South Korea continue to try to negotiate on tariffs while China warns them against making trade deals with the US that would be at the expense of China’s interests.

- 22 April - President Trump indicates that the 1_additional_rate tariffs on Chinese goods “won’t be that high” and will “come down substantially”, expressing hope that the Chinese President, Xi Jinping, would come to the negotiation table.

- 29 April - stock markets show signs of recovery, with the S&P 500 posting its best weekly gains since early April.

The most recent market rally appears to be primarily driven by optimism that the worst of the tariff escalation may be over. Investors have responded positively to signals that President Trump may be willing to negotiate and reduce tariffs, particularly with China. However, trade deals are yet to be agreed, and uncertainty remains about the long-term trade policy direction and its economic impact.

The clash between President Trump and the Federal Reserve also continues to cause concern about the central bank’s ability to run monetary policy independently:

- 21 April - President Trump calls on the Federal Reserve (the US central bank) to lower interest rates. His ongoing criticism of the Federal Reserve - and in particular its Chair Jerome Powell - causes further market instability.

- 22 April - President Trump doubles-down on his criticism of the Federal Reserve, but states that he has “no intention of firing” Jerome Powell.

The Federal Reserve is in charge of setting the nation’s interest rates - but it hasn’t lowered rates yet this year. President Trump called for lower interest rates in an attempt to offset the impact his tariffs are having on the likelihood of a recession. Lower interest rates make borrowing cheaper, stimulating demand and economic activity, but potentially pushing prices up. The Federal Reserve remains cautious about lowering interest rates as it risks causing a rise in prices (inflation), at a time where tariffs are already having an inflationary impact. The US interest rate range has remained unchanged at 4.25-4.5_personal_allowance_rate since December 2024. The Federal Reserve’s next board meeting takes place on 6-7 May.

The impact of Trump’s tariffs

Tariffs impact all countries as they make it harder to trade. That means companies could experience less growth and lower profits. When initial tariffs were announced, there was a sharp downturn across global stock markets due to many companies experiencing a decline in share price.

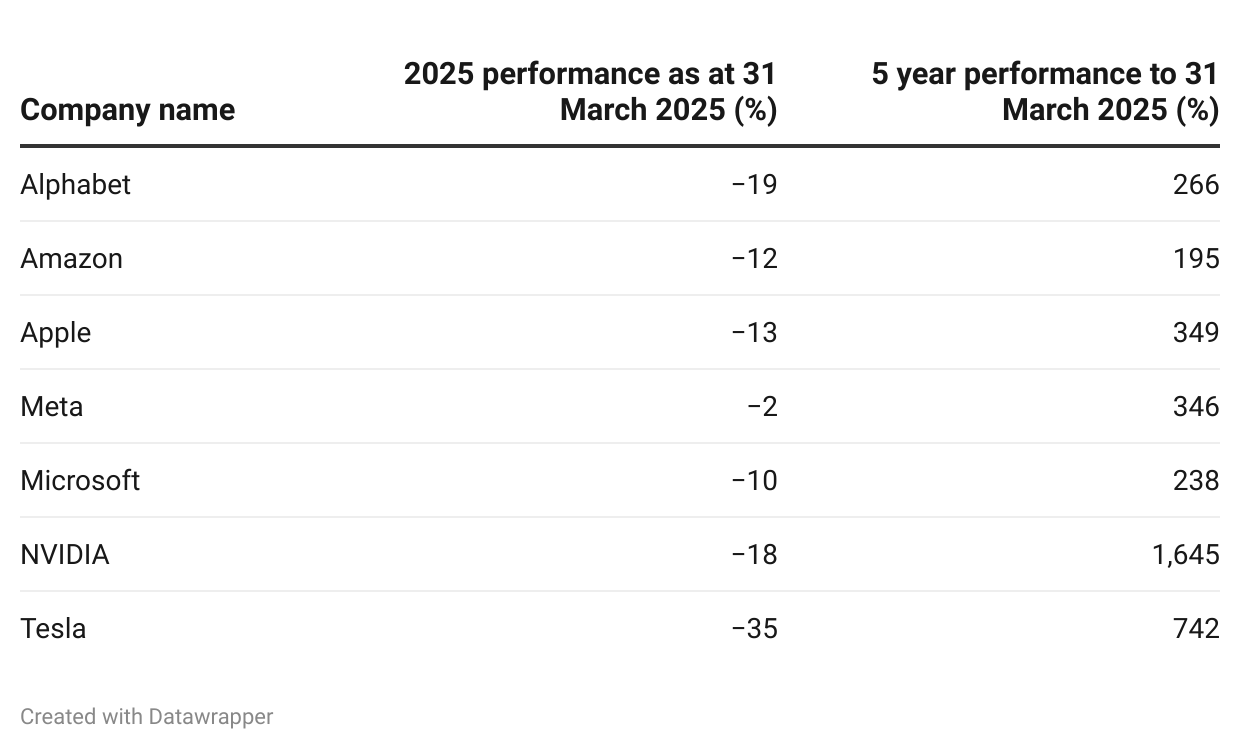

Seven leading US tech companies - also known as the Magnificent Seven - were particularly vulnerable to tariffs as a large number of their suppliers are based overseas. For example, Apple and Amazon both heavily rely on manufacturing and supply chains in China.

The Trump administration has since temporarily exempted smartphones, computers and certain other electronic devices from ‘reciprocal tariffs’, but has said that exemptions for technology from China could be short-lived.

While a partial stock market recovery occurred after the 90-day pause was announced, markets remain volatile. Financial markets don’t like uncertainty and can often react to news quickly, meaning sharp swings in the prices of company shares and bonds, which all pensions are invested in.

The table below shows recent performance data for the Magnificent Seven alongside their five-year performance. You can read more about Apple, Amazon, Meta, Microsoft and NVIDIA’s share prices in our new blog series to see how they might be affecting your pension balance.

Source: IBD data as of 31 March 2025 and MarketWatch 31 March 2020, 31 March 2025

So what does this mean for your pension?

We understand it can be worrying to see your balance fall, but history shows that markets do recover. It’s important to remember that pensions are designed for long-term growth. The Financial Conduct Authority (FCA) encourages pension savers to avoid making hasty decisions during periods of market turbulence. Staying invested and focused on the long term is usually the best course of action.

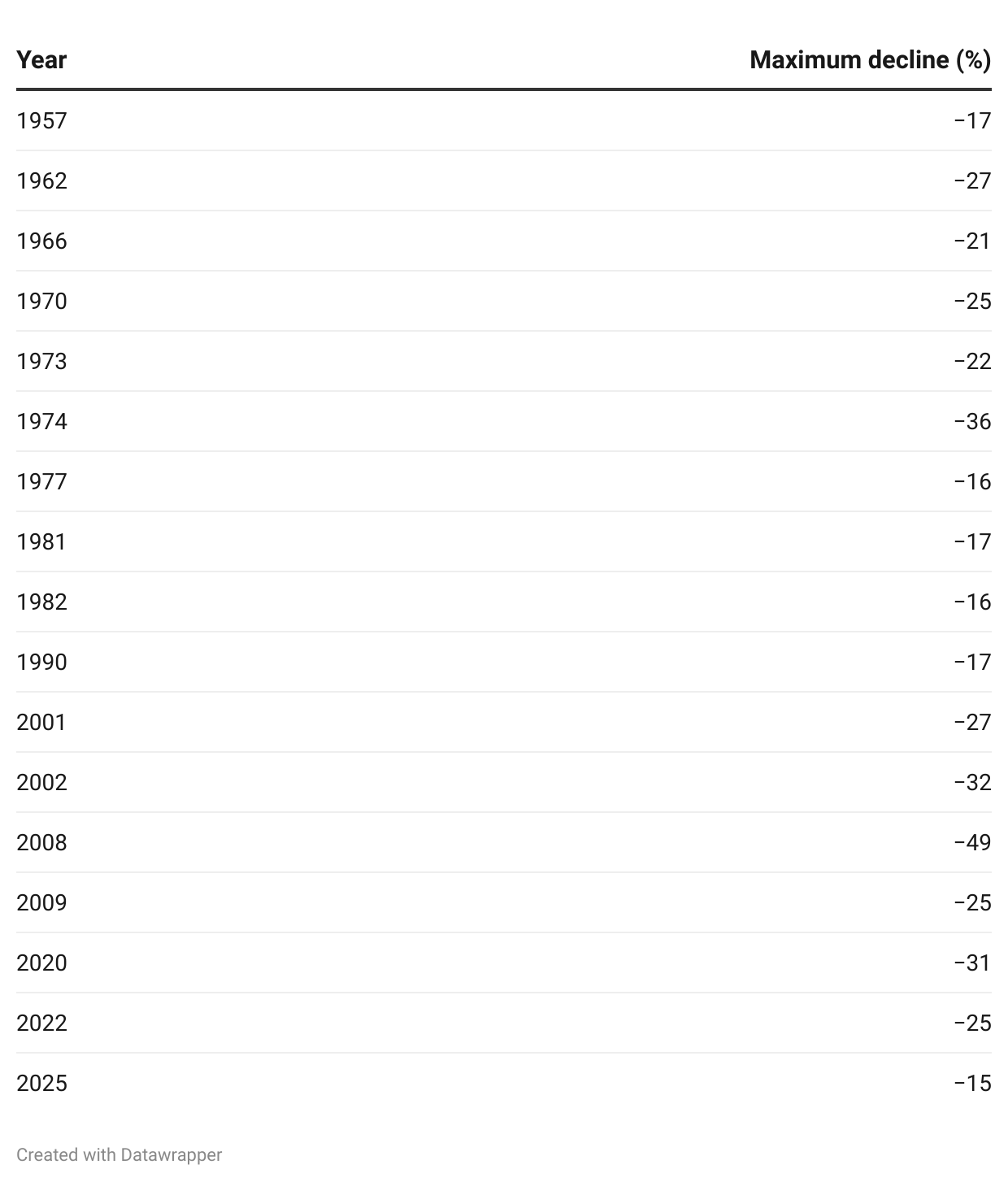

It’s important to remember that this kind of market volatility is normal during uncertain times, and it’s not unusual to see fluctuations day-to-day. When looking through history, we’ve seen many periods of fluctuation that look similar to this one. The exhibit below shows the maximum decline seen in historical years:

Source: Carson Investment Research, S&P 500 year-to-date move through April 8

Whilst past performance isn’t an indicator of future results, historical data shows that every decline in stock markets has been followed by a subsequent recovery and new historical highs. The chart below shows S&P 500 performance over the last 30 years.

Source: marcotrends

Why hasn’t my pension balance recovered yet?

The recovery of pension balances depends on how quickly global markets stabilise. This should start to happen once there’s more certainty around the economic changes proposed by President Trump. It’s also important to remember that your balance isn’t shown in real-time as it often takes several days to reflect market movements.

It might feel like there’s been a lot more volatility than usual over the last few years with the pandemic, the invasion of Ukraine, and now the uncertainty caused by tariffs. But historically, markets have always recovered from even bigger declines than we’re seeing now. That’s why the length of time that you’re invested in the market is so important. Staying invested means you’re in the best position to benefit and be part of the market recovery, when it comes. Keeping a cool head and thinking long term is key.

It may surprise you to learn that some investors would argue that downturns can provide a great opportunity to grow their investments, particularly if they increase their pension contributions during this time. That’s because the underlying value of each investment is lower, meaning investments go further and more units can be bought, leading to greater returns during market recovery.

Where to find pension information and support

Do you want to know more about your pension plan with PensionBee? You can check out our Plans page to learn how your money is invested in different assets and locations, or log in to your BeeHive to see your specific plan. You can always send comments and questions to our team via engagement@pensionbee.com.

Our default plans are designed to support you depending on your age.

If you’re under 50, our default is the Global Leaders Plan - a predominantly equity based plan that focuses on growth in your accumulation (or growth) years. The plan invests in around 1,000 of the world’s largest and most recognised public companies to offer a greater opportunity to grow pension savings before retirement.

If you’re over 50, our default is the 4Plus Plan which is designed for the decumulation (or withdrawal) years. This plan aims to achieve long-term growth of over 4% by investing your money into a mix of assets, including equities, bonds, cash and other asset classes. This plan is actively managed, meaning that the holdings may be adjusted weekly depending on market developments, as it seeks to balance growth and stability.

If you’re not sure where other pensions you may have are invested, you can usually find information online via your provider’s website or portal. Or, you can contact your provider and ask for a breakdown.

It could also be worth looking at resources like MoneyHelper. If you’re over 50, you can book an appointment with Pension Wise for free and impartial guidance.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |