This is part of our monthly global investment market update series. Catch up on last month’s summary here: What happened to global investment markets in June 2025?

President Donald Trump’s trade policies, particularly tariffs, remain a hot topic this summer. Tariffs are taxes on imported goods, and the US government has been using them to promote American businesses by making foreign products more expensive.

Some new trade agreements have been reached with the European Union and other countries, including the UK. But not everyone has been so lucky. Switzerland, initially facing a 31% tariff, had their rate driven up to 39% after negotiations failed to strike a deal. Meanwhile, India has been given the threat of a 5_personal_allowance_rate tariff starting from 27 August, unless they stop buying Russian oil.

The US economy has also been in the spotlight for other reasons. The US national debt has now reached around $37 trillion - the highest in the world. At the same time, there’s been a big decline in the value of the US dollar. Despite being the world’s reserve currency, it’s weakened against many other currencies including pound sterling. This has brought ‘US exceptionalism‘ into question once more.

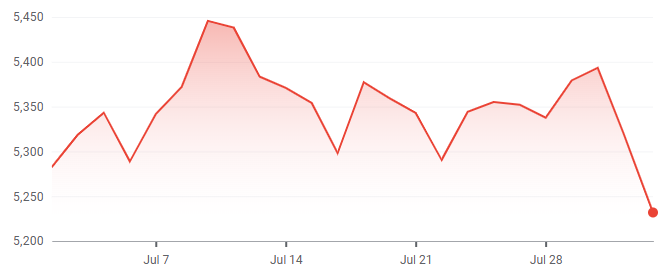

Tariffs have continued to cause uncertainty for global investors and sudden upticks or downturns in markets are to be expected. Despite this economic environment, markets have proved resilient. Investors are focussing on improved company earnings and hopes of lower interest rates. On 28 July, the S&P 500 (an index tracking 500 major US companies) hit a record high of nearly 6,390.

The index’s value is calculated by adding up the market values of all these companies, adjusting for their size, and then dividing by a special number called the divisor. For context, 2023 closed at 4,770 and 2024 closed at 5,882. This news boosted market confidence, with one asset management firm raising its year-end target for the S&P 500 to 7,100.

Keep reading to find out what these high US debt levels and a weaker dollar might mean for UK pension savers.

What happened to stock markets?

In the UK, the FTSE 250 Index rose by almost 2% in July. This brings the 2025 performance close to +7%.

Source: Google Market Data

In Europe (excluding the UK), the EuroStoxx 50 Index remained the same in July. This brings the 2025 performance close to +9%.

Source: Google Market Data

In North America, the S&P 500 Index rose by over 2% in July. This brings the 2025 performance close to +8%.

Source: Google Market Data

In Japan, the Nikkei 225 Index rose by over 1% in July. This brings the 2025 performance close to +3%.

Source: Google Market Data

In the Asia Pacific (excluding Japan), the Hang Seng Index rose by almost 3% in July. This brings the 2025 performance close to +24%.

Source: Google Market Data

What’s happening in the US economy?

The US economy is going through some big changes this year and these shifts are being felt around the world. Here’s a simple look at what’s happening and what it means for UK pension savers.

US debt is on the rise

The US national debt has reached about $37 trillion, the highest in its history. When a country owes this much, it has to spend more just to pay the interest on its loans. This leaves less money for things like public services or investment. High debt also makes some investors worry about the US’s ability to pay it back and what impact that may have on American companies. These concerns could lead to uncertainty in financial markets, both in the US and abroad, which may make pension balances more volatile.

The value of the US dollar is falling

The US dollar is important because it’s used in trade all over the world. Recently, it has been losing value against other major currencies, like the pound. A weaker dollar means American goods are cheaper for buyers in other countries. But it also means the US has to pay more for imports. When the dollar drops, it can be a sign that investors are less confident in the US economy. For the UK, this means the value of investments tied to the dollar, presented back in pound terms, can go down, even if the investments are doing well in their local currency (the dollar).

What impact does this have on UK pensions?

What does ‘hedging’ mean?

If you look outside and the sky looks cloudy, you might take an umbrella just in case it rains. The umbrella won’t stop the rain, but it’ll keep you dry if the weather changes. In this example, your pension is like you, and the currency change (like the US dollar going up or down) is the rain.

If your pension is ‘hedged’, it’s like having that umbrella. It helps shelter your savings from sudden currency swings, keeping things more steady. If your pension is ‘unhedged’, it’s like leaving the umbrella behind. You’re fully exposed to all the sunshine and rain the day brings (in this example, the ups and downs of a currency).

But umbrellas, just like hedged funds, aren’t free. For pension savers over 50 years old, or those withdrawing an income from their pension, these currency swings may be more visible in your pension balance. That’s why it’s more common to see hedging on pension funds designed for people in this stage of retirement.

For pension savers under 50, these currency fluctuations usually won’t impact your long-term goals. As strange as it may sound, contributing to your pension when the US dollar is weak against pound sterling can even be cost-effective. That’s because your pounds are able to buy more goods in dollars (in this case, company shares).

Which PensionBee plans contain hedging?

This information is accurate as of the date of publication.

Have a question? Get in touch!

Do you want to know more about your pension plan with PensionBee? You can check out our Plans page to learn how your money is invested in different assets and locations, or log in to your BeeHive to see your specific plan. You can always send comments and questions to our team via engagement@pensionbee.com.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |