This is part of our monthly pension update series. Catch up on last month’s summary here: What happened to pensions in November 2023?

2022 ended with stock markets bruised and battered, grappling with inflation’s relentless grip on the global economy. Enter 2023, a year that promised little but delivered much - surprising experts and investors alike. It was a tale of two halves, marked by unexpected pivots and record-breaking rebounds.

In the first half of 2023, a recovery began. This was cut short in March when three midsized US banks collapsed within a week. The coverage from news outlets drew several parallels to the 2008 financial crisis which led to the Great Recession. As fears grew, share prices shrunk. But by May it was back to “business as usual”.

In the second half of 2023, the rollercoaster effect returned. Earnings season in July, where publicly-listed companies publish their performance, signalled more market resilience than expected. By October, concern over central banks raising interest rates returned and share prices dipped again - only to rebound to greater heights.

Keep reading to find out how global stock markets performed in 2023 and what investors can hope for as we begin 2024.

What happened to stock markets?

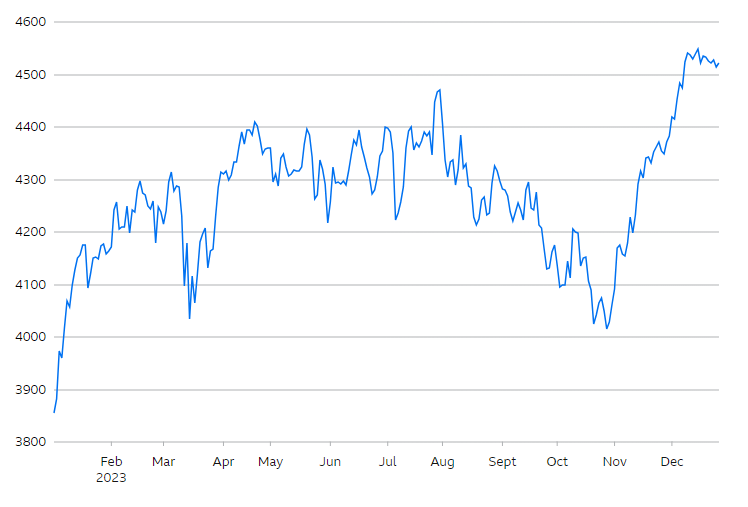

In UK stock markets, the FTSE 250 Index rose by a remarkable 8% in December. This brings the 2023 performance to +4.4%. This is a favourable performance when compared to the UK’s largest market stalwarts, known as the FTSE 100 Index, which delivered a 3.8% return to investors in 2023.

While the +4.4% return is encouraging, it’s worth noting the FTSE 250 currently only has a cumulative 5-year return of +12.5%. This raises questions about whether December marks the start of an upward trend, or was only a temporary boost to an otherwise gentle growth path.

Source: BBC Market Data

Across the English Channel, the EuroStoxx 50 Index rose by over 3% in December. Unlike the FTSE 250, it wasn’t a December surge that defined the year, but rather a marathon of ups and downs. By the end of 2023, the index had a performance close to +19.2%. This level of annual growth is rarely seen outside of the US.

Over the past five years we’ve seen the EuroStoxx 50 rise by 50.7%. This demonstrates an underlying strength and innovation within the region’s corporate landscape, hinting at potential for further growth once the dust settles on recent economic volatility.

Source: BBC Market Data

The biggest stock market present in the majority of investment savings (including UK pensions) is the S&P 500, based in the US. This is because historically it has outperformed other stock markets by a wide margin. The S&P 500 Index rose by over 4% in December, bringing the 2023 performance close to +24%.

While many US companies are still floundering, the “Magnificent Seven” carried the S&P 500 to a triumphant finish line, with annual returns ranging from +_scot_top_rate (Apple) to +239% (Nvidia). Over the past five years we’ve seen the S&P 500 rise by 90.3%, one of the strongest global returns.

Source: BBC Market Data

Unfortunately, not every stock market enjoyed modest to magnificent returns. The Chinese-based Hang Seng Index remained stagnant in December, bringing the 2023 performance close to -14%. Although China and the US are the largest economies in the world, the performance of their stock markets have only widened in distance.

After decades of growth, the Hang Seng has failed to maintain that momentum in recent years. Over the past five years we’ve seen the Hang Seng fall by 34%. Reasons for this underperformance vary from a real estate crisis to strained US-China relations.

Source: BBC Market Data

How did the investment landscape shift in 2023?

Inflation and interest rates seesaw

There’s an interconnected relationship between inflation and interest rates; often when one is high, the other will rise and vice versa. Stable inflation and interest rates are integral to growing the prosperity of a country. The difficulty occurs when one experiences instability and becomes too high or low. It’s the job of central banks, such as the Federal Reserve in the US and Bank of England in the UK, to adjust interest rates to temper inflation.

By the end of 2023, it looked like inflation may have peaked. As of December, the UK’s rate of inflation was at a 12-month low of 3.9%, and interest rates were holding steady at 5._corporation_tax. If central banks continue to pause the interest rate hikes, or even begin lowering rates, this could further boost investments. Conversely, the current appetite for cash savings may lessen if interest rates fall.

Company shares divided opinions

Company shares are units of ownership in a company. When a company wants to raise money, it can issue shares to investors who pay a certain amount of money for each share. By buying shares, investors become part-owners of the company and can enjoy its profits or growth. But, they also take on the risk of a decline in share prices if the company performs poorly or even goes bankrupt.

In the face of rising rates and inflation, company shares became very sensitive to economic optimism and pessimism. Usually, public companies announce their performance every three months and investors react to this news, shifting the share price dependent on the update. In 2023, investors also had to consider the impact of the wider economy and interest rates on future profitability and company balance sheets.

Bonds on the mend

Bonds are a type of investment where you lend money to an organisation, like a government or company. In return, they agree to pay you back with interest over a period of time. A bond yield is the annual return that an investor gets from a bond. Due to their historical stability and predictability, bonds are a popular choice for shorter-term investors such as retirees who plan to drawdown in the near future.

As interest rates peaked in 2023, a curious phenomenon arose: bonds started looking attractive again. After years of near-zero returns, the fixed income offered by bonds provided a safe haven in the stormy equity market. Investors, seeking to weather the turbulence, flocked to bonds. For some, it was a return to a long-forgotten asset class, a welcome respite from the stock market’s rollercoaster.

What does this mean for pensions?

2023 was a prosperous year for many global stock markets and many pension savers will have seen growth in their retirement savings. It may well seem we’re now on the path to recovery. Nevertheless, geopolitical and economic tensions around the world remain high, and with elections looming in several countries, including the UK, there’s still potential for future turbulence. In any case, pension saving is usually a marathon and years like 2023 make saving productive in the long run.

You can check out our Plans page to learn how your money is invested in different assets and locations. You can always send comments and questions to our team via engagement@pensionbee.com.

This is part of our monthly pension update series. Check out the next month’s summary here: What happened to pensions in January 2024?

Have a question? Get in touch!

You can check out our Plans page to learn how your money is invested in different assets and locations. You can always send comments and questions to our team via engagement@pensionbee.com.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |