This is part of our monthly pension update series. Catch up on last month’s summary here: What happened to pensions in September 2023?

With the Autumn Budget due in November and a general election on the horizon next year, all eyes are on the UK government. There’s growing speculation that the current government may permanently change the State Pension ‘triple lock‘. This is a policy that guarantees that the State Pension will rise each year by the highest of three measures: inflation, average earnings growth, or 2.5%.

Introduced in the 2011/12 tax year, the triple lock has been a popular policy with pensioners as it’s helped to ensure that their incomes have kept pace with the cost of living. However, the triple lock has come under criticism from some who have claimed it’s become too expensive for taxpayers to maintain, particularly in light of recent economic volatility.

If the State Pension keeps rising as intended, it could cost the taxpayer more than education, policing and defence combined by 2025. The government could alter it to a lower rate, or even abolish it altogether, to save taxpayer money.

Keep reading to find out how markets have performed this month and why the State Pension triple lock is making headlines again this Autumn.

What happened to stock markets?

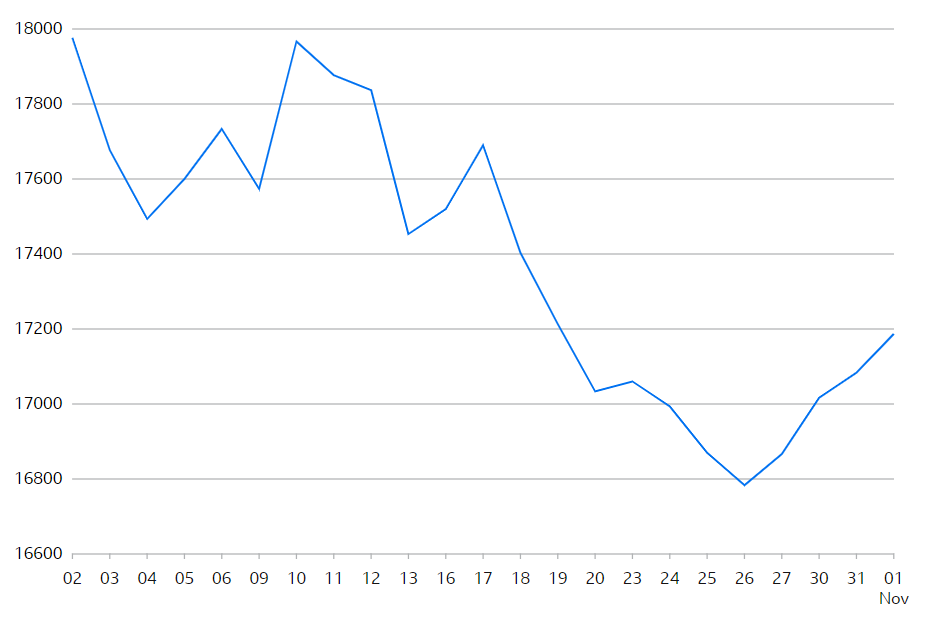

In UK stock markets, the FTSE 250 Index fell by almost 7% in October. This brings the year-to-date performance close to -9%.

Source: BBC Market Data

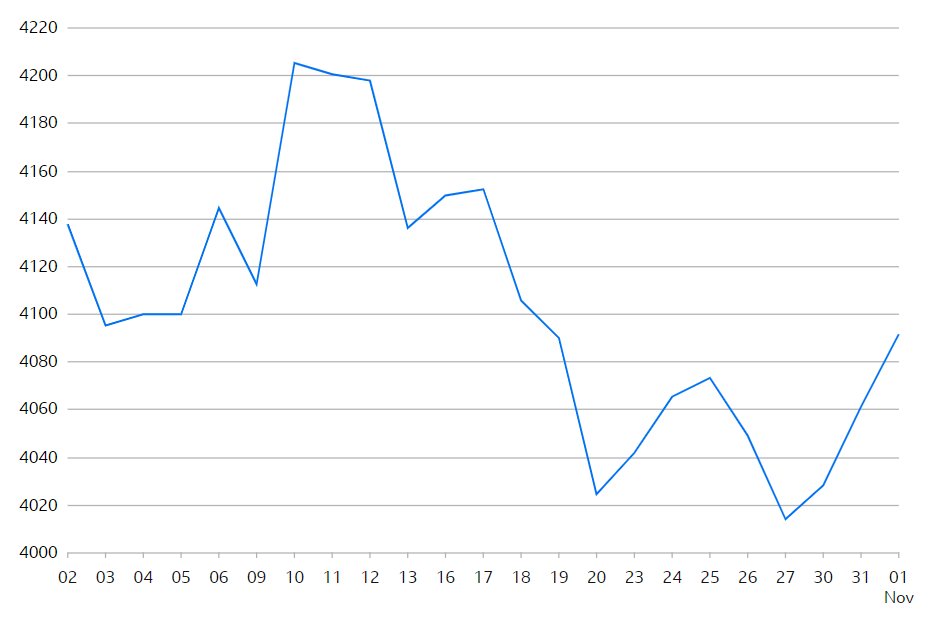

In European stock markets, the EuroStoxx 50 Index fell by almost 3% in October. This brings the year-to-date performance close to +7%.

Source: BBC Market Data

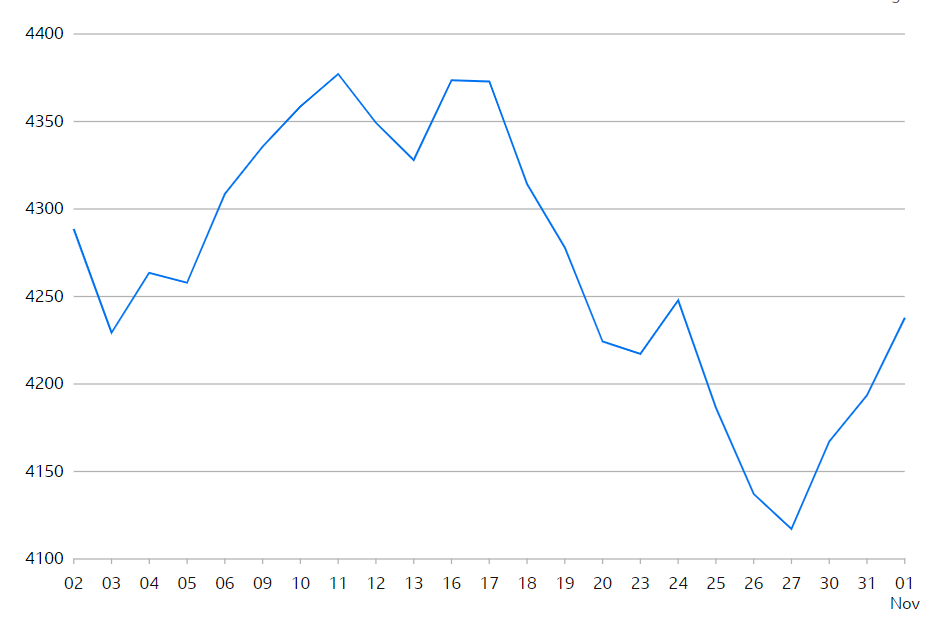

In US stock markets, the S&P 500 Index fell by over 2% in October. This brings the year-to-date performance close to +9%.

Source: BBC Market Data

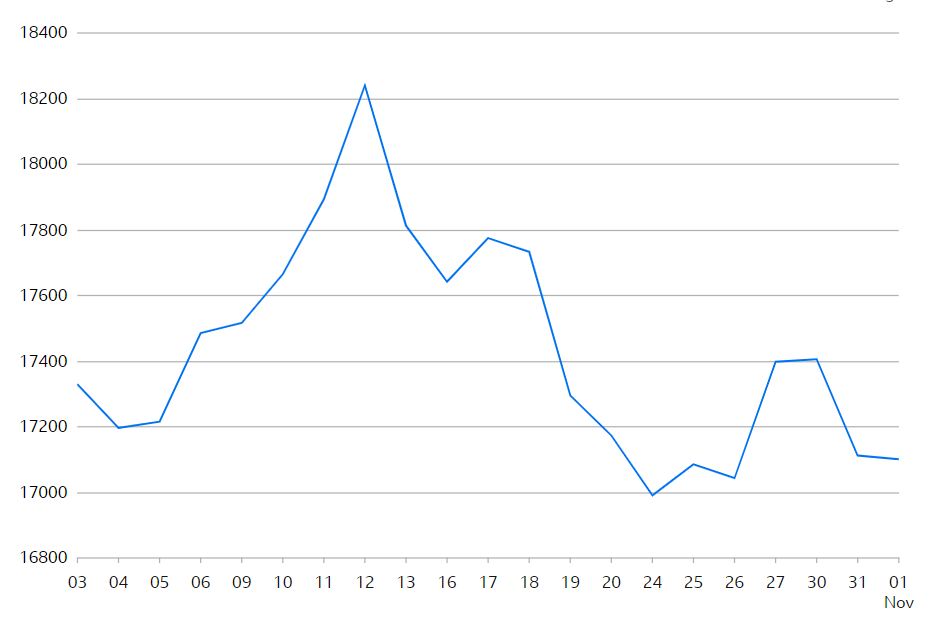

In Asian stock markets, the Hang Seng Index fell by almost 4% in October. This brings the year-to-date performance close to -14%.

Source: BBC Market Data

Triple lock: set to rise, or under threat?

Under the triple lock policy, the State Pension should increase each April by the highest of the following three measurements:

- inflation, as measured by the Consumer Price Index (CPI) in the September before;

- average earnings growth, as measured by the Office for National Statistics (ONS) in the September before; or

- 2.5%, as the minimum annual increase.

This annual increase applies to both the basic State Pension (pre-April 2016 retirees) and the new State Pension (post-April 2016 retirees).

How much could the State Pension increase by?

In April 2023, the State Pension increased by 10.1% due to the rise in inflation. This resulted in:

- the new State Pension increasing to £203.85 a week (equivalent to around £10,600 a year) for the 2023/24 tax year; and

- the basic State Pension increasing to £156.20 a week (equivalent to around £8,122 a year) for the 2023/24 tax year.

In April 2024, the State Pension in theory should increase by 8.5% because of the rise in average earnings. This would result in:

- the new State Pension rising to £221.20 a week (equivalent to around £11,502 a year) for the 2024/25 tax year; and

- the basic State Pension rising to £169.50 a week (equivalent to around £8,814 a year) for the 2024/25 tax year.

Why’s the triple lock under threat?

In October, during the Conservative Party conference Prime Minister Rishi Sunak announced the scrapping of the high-speed northern rail line due to spiralling costs. With the Autumn Budget around the corner, the Chancellor Jeremy Hunt is under pressure to cut public spending and there are two key benefits at risk.

First, freezing working-age benefits to save £4 billion. This would be a controversial move during a cost of living crisis. It could also be seen as a political betrayal of the government’s promise to “level up” the country.

Second, altering State Pension benefits. For the _tax_year_minus_three tax year, the government intervened and suspended the triple lock guarantee - saving an estimated £3 billion. If the government were to alter State Pension benefits further, this would have a significant impact on the retirement incomes of older people.

Is the triple lock policy fair?

One of the main arguments in favour of scrapping the triple lock is that it’s unfair to younger generations. The UK’s State Pension works like a cash machine, where taxpayers deposit money through National Insurance contributions and retirees withdraw money through State Pension entitlement.

This model becomes problematic when combined with an ageing population and falling birth rate. The cost of funding the State Pension will fall increasingly on younger generations, who will have to pay higher taxes during their working life without any guarantee of receiving State Pension benefits when they retire.

Am I on track to retire comfortably?

Currently both eligible men and women can claim their State Pension benefits from the age of _state_pension_age, but for those born after 5 April 1960 it’ll rise to _pension_age_from_2028 by 2028. It’ll eventually rise to 68, affecting those born after April 1977. You can discover if you can afford to retire before your State Pension age with our State Pension Age Calculator.

Even if the triple lock is kept, it’s important to remember that it doesn’t guarantee a comfortable retirement. According to the Pensions and Lifetime Savings Association’s (PLSA) Retirement Living Standards you’d need £23,300 a year to afford a moderate retirement if you’re single and £34,000 a year as a couple.

There are several ways to save for retirement without relying on the State Pension, including your workplace pension or saving into a personal pension. Aiming for a happy retirement? Become a pension pro in just 30 minutes, with our Pension Academy video series hosted by Patricia Bright, a lifestyle and finance influencer.

This is part of our monthly pension update series. Check out the next month’s summary here: What happened to pensions in November 2023?

Have a question? Get in touch!

You can check out our Plans page to learn how your money is invested in different assets and locations. You can always send comments and questions to our team via engagement@pensionbee.com.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |