This article was last updated on 20/04/2026

Get your retirement planning off to a great start by checking your State Pension forecast. The State Pension may not be megabucks, but it’s definitely worth discovering how much you’ll get and when, as this can vary. Read on for a step-by-step guide to get your forecast.

How much is the State Pension?

The State Pension is regular money you get paid by the government after reaching retirement age. This is currently 66 and rising to 67 in 2028, and the amount you’ll get depends on your National Insurance record. The full new State Pension is currently £241.30 a week, which tots up to just over £12,547 a year for tax year 2026/27, and it goes up every April. Right now the government is committed to pushing it up each year due to the triple lock on the State Pension by whichever is highest of three figures:

- average earnings growth;

- inflation based on the Consumer Price Index (CPI); or

- 2.5%.

It’s worth noting that you only get the full whack if you’ve racked up enough National Insurance contributions, whether as payments while working, or as credits while unable to work, for example when receiving certain benefits or caring for children under 12. Typically you need at least 10 ‘qualifying years’ on your National Insurance record to get anything, and you need 35 qualifying years to get the whole lot.

When will I get my State Pension?

Right now, State Pension payments kick in from the age of 66, unless you choose to delay it, but that retirement age is a moving target. It’s due to increase to 67 by 2028, and to 68 by 2046, although the government has been murmuring about whether to speed up the increase to 68. If you’re not sure what age you’ll be able to access your State Pension, PensionBee’s State Pension Age Calculator can help.

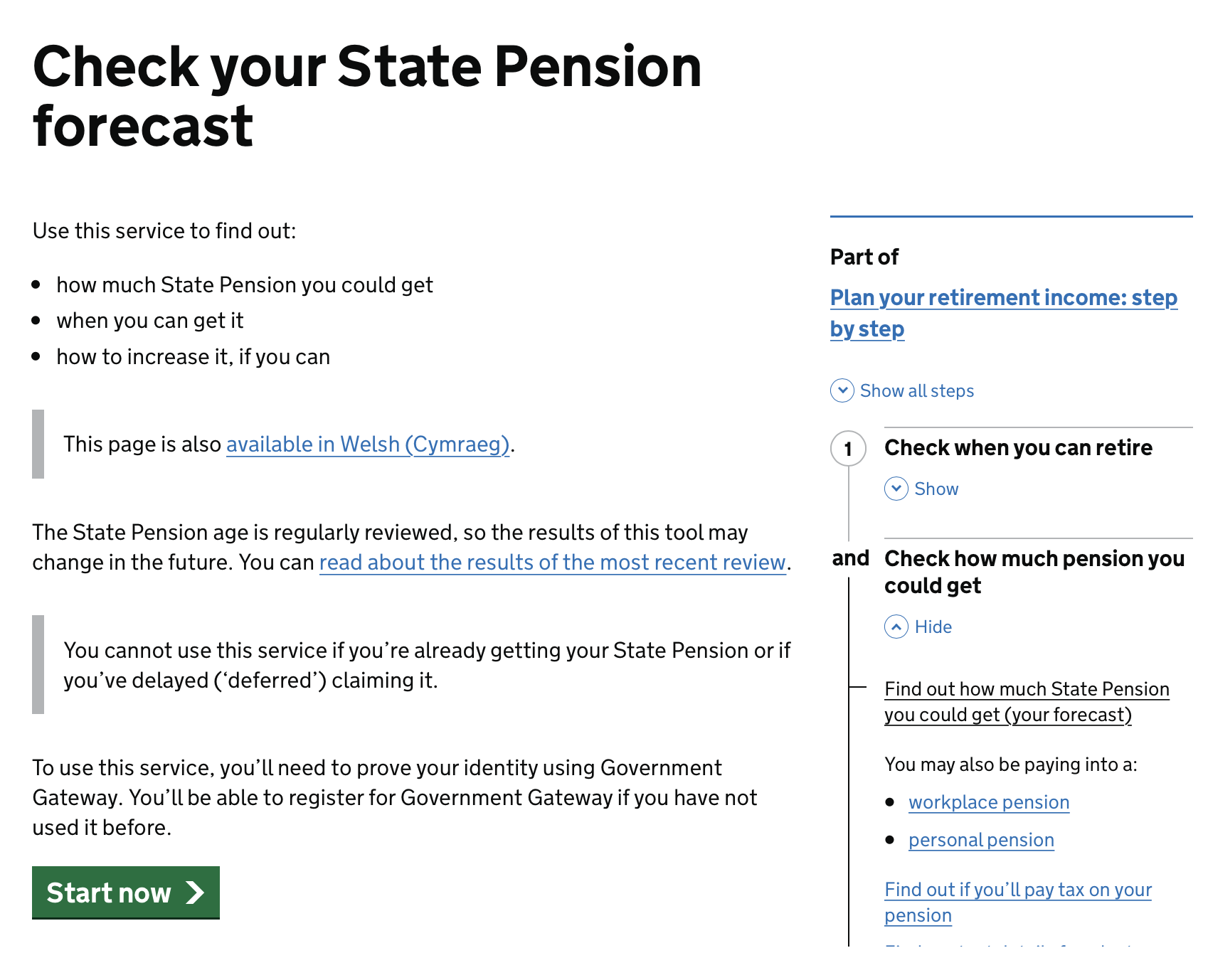

How can I check my State Pension forecast?

The easiest way is to head online. But if you’re at least 30 days away from State Pension age, you can also fill in a BR19 application form and send it by post, or request a forecast from the Future Pension Centre on 0800 731 0175 or 0800 731 0176. You can ask the Future Pension Centre to send you a copy of a BR19 form too.

Pop in your Government Gateway details

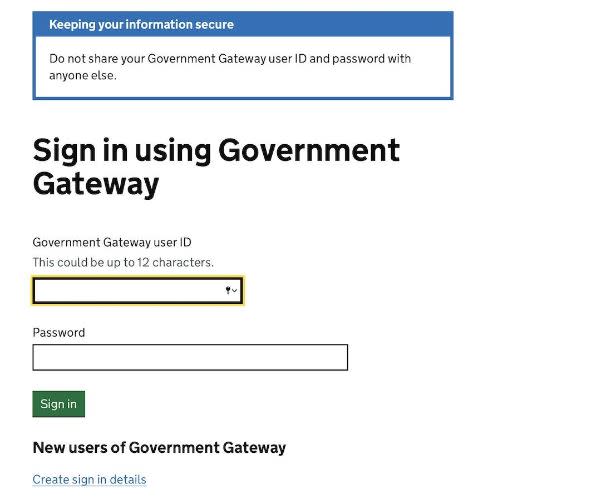

To access your State Pension forecast online, click on ‘Start now’ and then put in a Government Gateway user ID and password. If you’ve ever filed a Self-Assessment tax return online, you’ve probably already got these details.

Creating a Government Gateway account

If you don’t already have a Government Gateway account, you’ll need to click on the link to ‘Create sign in details’, put in your email address and pop in the code sent to your email address. If you then enter your name and create a password, it’ll generate a Government Gateway user ID. Make sure you print out your user ID or make a note of it somewhere safe.

If you’re doing this to check your State Pension forecast, click on the option to set up an individual account, decide how you want to receive verification codes and then verify your identity (you’ll need your National Insurance number to hand).

Usually, you can choose between answering questions about your passport or information from your payslips or a recent P60. If you can’t, you can opt for questions based on your credit report – so about bank accounts, mobile contracts, loans, past addresses and so on.

{{main-cta}}

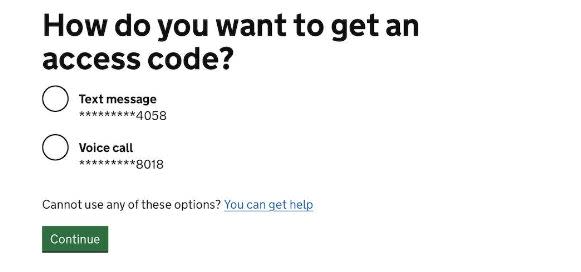

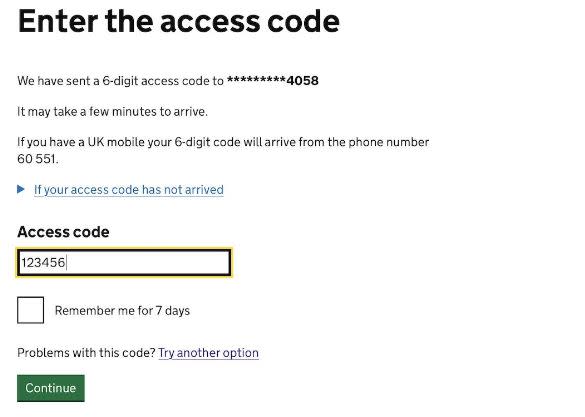

Accessing the Government Gateway

Once you’ve entered your Government Gateway user ID and password, you’ll be asked to choose how to get an access code, whether by text or a phone call.

Select the option you prefer, click ‘continue’ and then pop in whatever six digit code you get sent:

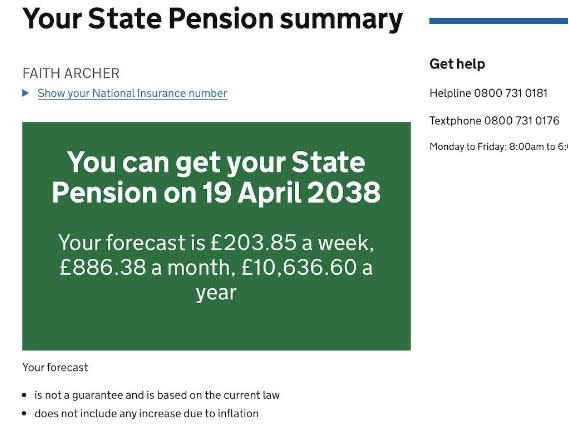

View your State Pension summary

Bingo, you’re through to your State Pension summary! At the top, it tells you the date your State Pension is due to start, and how much pension you’re forecast to get by then. The amount is based on current State Pension payments, rather than guessing how much the State Pension will be in years to come. As it says, there’s no increase based on inflation, but you can weigh up what the forecast would buy at today’s prices.

The screen grab shows my forecast, and (many cheers) it looks like I’m on track to get the full amount.

State Pension based on National Insurance contributions (NICs)

Scroll down your forecast, and you’ll see how much State Pension you’re entitled to based on your current National Insurance record, and how many more years you need to contribute to get a higher State Pension. Thankfully, I only need to pay NICs for another four of the next 15 years before April 2038 to qualify for a full new State Pension, which sounds eminently possible. Sadly, I won’t be able to stop paying NICs as soon as I qualify for the whole lot – if I keep on working, I’ll have to keep paying NICs right up until I hit the State Pension age.

Scrolling further down reveals the caveat that, although I’m currently due to reach State Pension age in 2038, this may increase by up to a year.

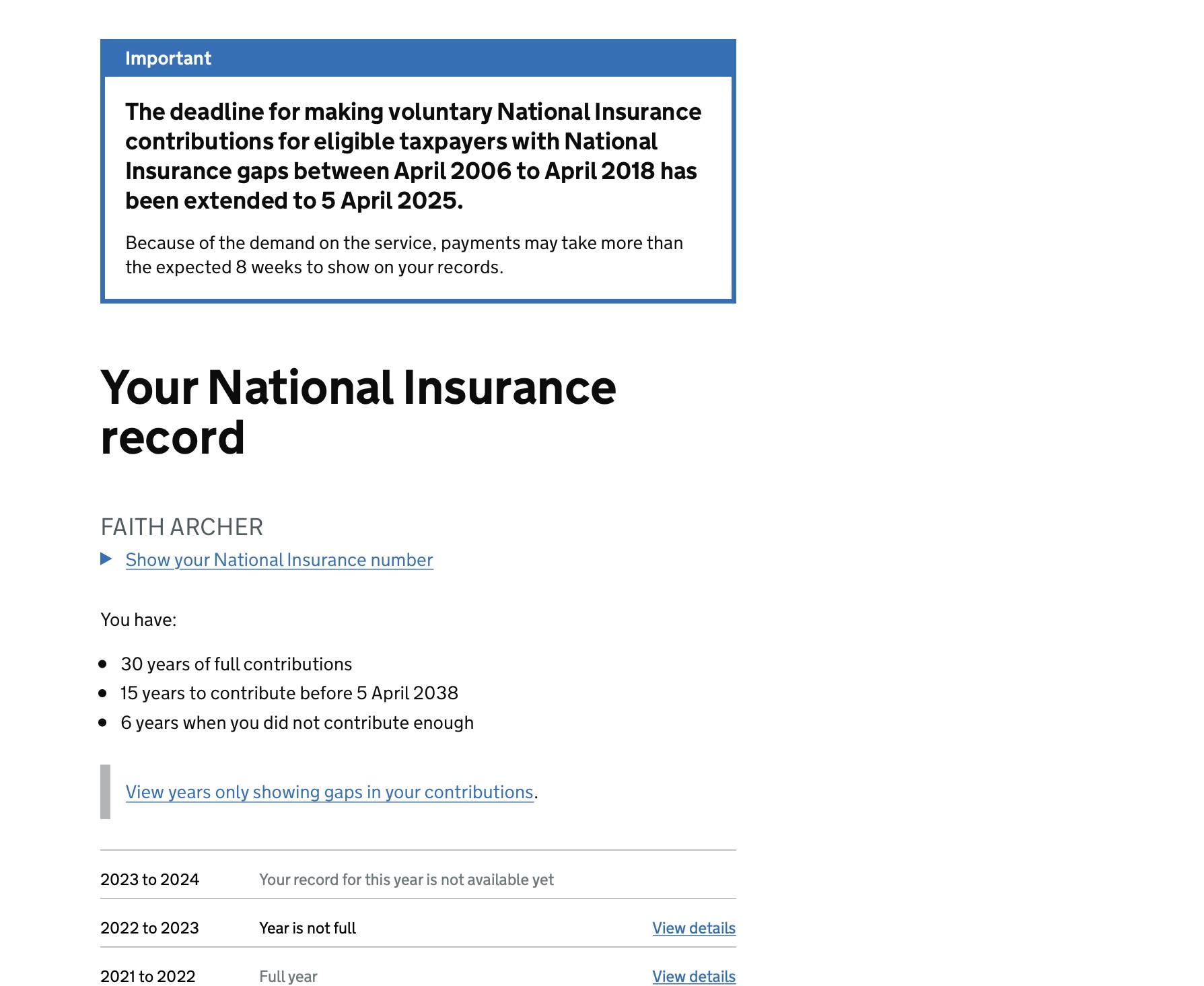

View your National Insurance record

It’s worth clicking on ‘View your National Insurance record’, as this lists all your NICs by year, including whether you have full years or didn’t contribute enough.

Remember how you need 35 qualifying years to get the maximum State Pension?

If you have gaps in your National Insurance Record, you might consider making extra payments to qualify for more pension. Normally, you can only make voluntary contributions to fill any gaps in the previous six years. However, until April 2025, there’s the chance to make up the difference much further back, for years between April 2006 and April 2018. This potentially applies to men born after 5 April 1951 and women born after 5 April 1953.

Don’t assume you have to top up any gaps. If you’ve got loads of time before retirement, and will easily rack up the 35 years needed before then, it’s probably not worthwhile. But if, for example, you’re close to retirement but aren’t on track for a full State Pension, or have years which would be super cheap to top up because you only missed out by a few weeks, it could be worth plugging some gaps.

Give the Future Pension Centre a call on 0800 731 0175 if you haven’t yet reached State Pension age, and want to find out if you’ll get more pension by paying for extra years. I have six years when I didn’t contribute enough, while I was at university and during a year out. But my gaps were too long ago to top up, and it wouldn’t be worth paying anyway, as I only need to rack up five years of NICs during the next 15 to get the maximum State Pension.

Checking your State Pension forecast sooner rather than later gives you the chance to plug any gaps before it’s too late, as well as discovering how much you’re likely to get and when.

Faith Archer is a Personal Finance Journalist and Money Blogger at Much More With Less.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |