This is part of our monthly pension update series. Catch up on last month’s summary here: What happened to pensions in August 2022?

Pensions are invested in global stock and debt markets, and therefore what happens around the world will also be felt in our pensions. September saw the continuation of the domino effect created by the international energy crisis and the ongoing war in Ukraine. The combination of low energy supplies, and high demand for them, has pushed prices upwards. These costs are passed from business to consumer, making the cost-of-living higher and increasing wages, which in turn leads to higher demand for goods and higher prices. In short, a vicious cycle that the world’s central banks have sought to break through rising interest rates.

Of course, rising interest rates themselves can cause a lot of turmoil for businesses and households by increasing the cost of borrowing and reducing expenditure. This in turn reduces inflation (by reducing the demand for goods) but can simultaneously lead to business closures and job losses, which September continues to bring news of. At the same time, rising interest rates reduce bond prices, meaning diversification of pension assets is less effective in the short-term.

Keep reading to find out how markets have performed this month, and how this may impact your pension balance.

What happened to stock markets?

Company shares are traded on stock markets, and their value’s influenced by all sorts of factors, including: a changing political climate, business performance, interest rates, local and global economies and the rate of inflation.

September marked a subsequent chapter in this year’s unfolding story of market volatility. Uncertainty over measures taken by central banks to combat inflation (interest rate rises), along with the energy crisis, has clouded any optimism for an imminent recovery.

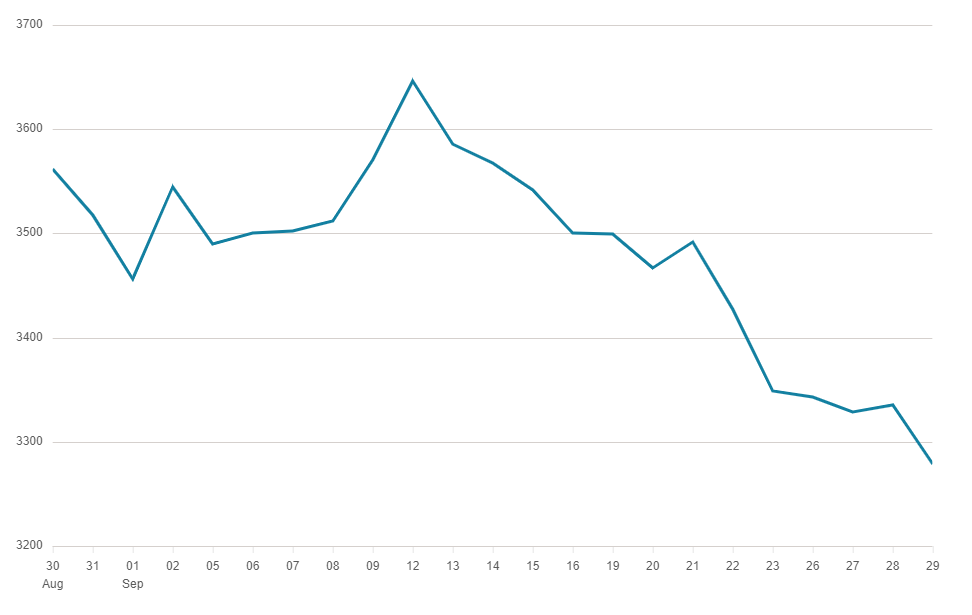

In UK stock markets, the FTSE 250 Index fell by over 1_personal_allowance_rate in September, bringing the year-to-date performance close to -29%.

Source: BBC Market Data

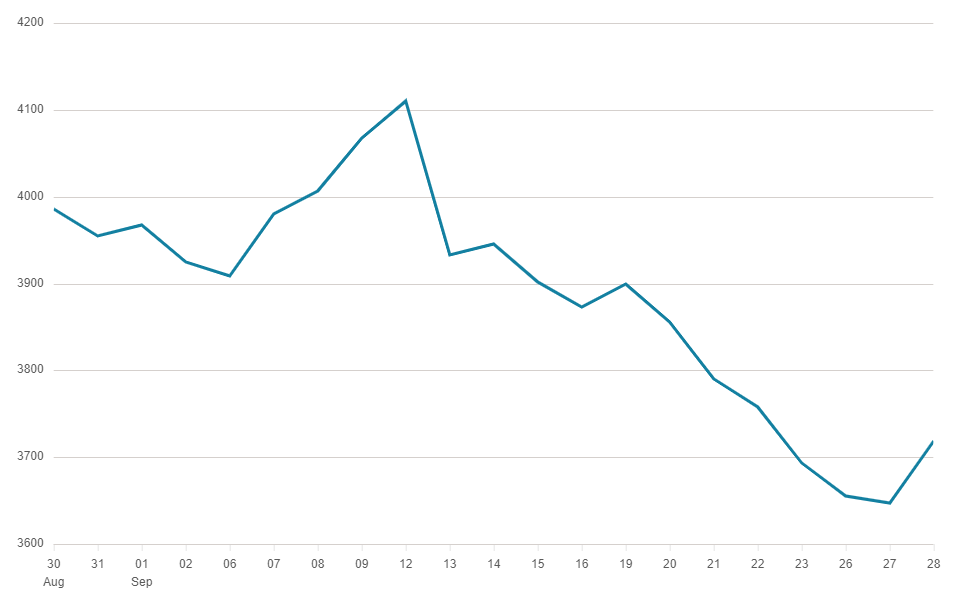

In European stock markets, the EuroStoxx 50 Index fell by almost 6% in September, bringing the year-to-date performance close to -24%.

Source: BBC Market Data

In US stock markets, the S&P 500 Index fell by almost 8% in September, bringing the year-to-date performance close to -24%.

Source: BBC Market Data

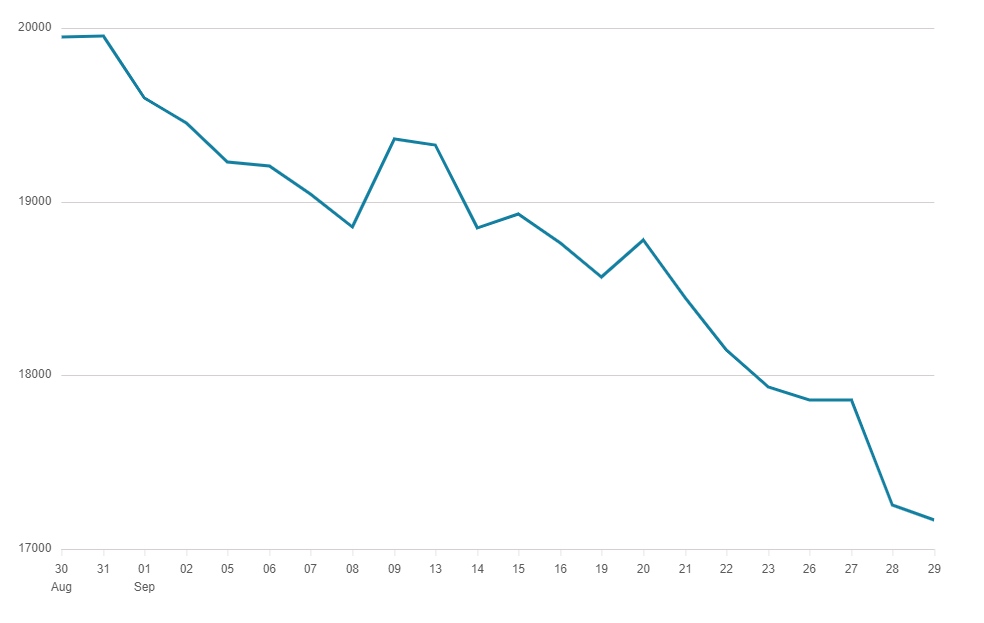

In Asian stock markets, the Hang Seng Index fell by over 12% in September, bringing the year-to-date performance close to -26%.

Source: BBC Market Data

What happened to currencies?

Currency is a system of money commonly attached to an economic region or an individual country. For example, in the UK our currency is pound sterling. As currencies fluctuate in value they’re often phrased as being ‘strong’ or ‘weak’, compared to others. Exchange rates are those points of comparison, as you move money from one currency to the equivalent buying power in another.

September saw pound sterling fall by almost 5% against the Euro, by almost 4% against the Japanese Yen and by almost 8% against the US Dollar. This reflects the UK’s weaker economic outlook, as inflation is hovering at 9.9%. In reaction to the rise in inflation, the Bank of England raised interest rates to 2._corporation_tax. There’s speculation about further rises in coming weeks, at time of writing.

Customarily funds, such as pensions, invest internationally as part of diversification, the approach of spreading your investment eggs in more than one basket. Chances are many UK investors hold more of their retirement wealth in US companies than UK companies. Therefore, it’s possible to have benefited from a falling pound in your pension.

However, if you’re close to retirement or if your fund manager uses ‘currency hedging‘ as a way of reducing volatility, you’ll be protected from negative currency moves on your overseas investments (such as a weakening of the US Dollar), but also won’t benefit from positive ones (such as a strengthening of the US Dollar).

You can read our blog, The pound and its impact on pensions, to learn more.

What happened to bonds?

Bonds are basically loans given by investors to companies. In exchange for their funding, the company usually pays investors fixed interest on the bond amount before repaying it in full. Bonds have different characteristics (like mortgages) from their interest rates to their term length. There are two types of bonds: corporate and government.

Like many fixed income assets, bonds thrive on market stability as they aim to provide moderate growth for investors. Recent surges in inflation and rising interest rates have pushed bonds between the proverbial rock and a hard place - leaving investors understandably concerned. While asset classes such as company shares are used to the ups and downs, bonds have been relatively sheltered from volatility until this point.

At the time of writing, the S&P Global International Bond Index is reporting over 3_personal_allowance_rate losses this year alone. The downside is obvious; investments that are bond-heavy will have seen dramatic losses. Bond’s haven’t seen losses this severe since back in 1865. Since 1939, when the Great Depression ended, the bond market has created annual returns of approximately 5%, overtaking the rate of inflation by a slim margin in most years.

The upside is that hopefully we’ll recover some or all of these falls in the medium-term, and not see double digit losses like we currently are for another 200 years, give or take. Many pension funds will be diversified, including investments in bonds and shares. It’s impossible to completely isolate your retirement savings from the wider economy - even investing in cash means you could lose value due to inflation.

You can read our blog, How does inflation affect pensions?, to learn more.

Summary

We’re currently in a bear market (a period of economic decline). The good news is global markets have recovered from every bear market in history, without exception. Moreover, the value of company shares has not only recovered but typically goes on to reach new highs. Even the biggest market crash since the Great Depression, the 2008 global financial crisis, was followed by the longest period of sustained growth in market history until the coronavirus pandemic struck markets in 2020.

As a general rule of thumb, when markets are down company shares become more affordable to investors. For example, if you buy company shares during a downward trend at £1 per share, then when markets recover and they increase to say £1.50, you’ll have seen a 5_personal_allowance_rate increase on your initial investment. Of course, there’s no guarantee that this will happen, but if you’re able to, then adding to your pension pot could allow you to effectively grow your pension in the long term.

You may find yourself rethinking your pension savings during the cost of living crisis, or worrying about whether you’re making the right choices. PensionBee customers can rest assured knowing that our pension plans are being managed by some of the world’s leading money managers. Again, it’s worth remembering that it’s normal and expected for pensions to go up and down in value. If you’re over the age of 50 and are considering your retirement options, you may benefit from a free Pension Wise appointment. You can book your appointment online.

This is part of our monthly pension update series. Check out the next month’s summary here: What happened to pensions in October 2022?

Have a question? Get in touch!

You can check out our Plans page to learn how your money is invested in different assets and locations. You can always send comments and questions to our team via engagement@pensionbee.com.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |