It can be worrying to see the value of your retirement savings move up and down with such unpredictability. And if you’ve been keeping an eye on your pension in January, you might have experienced more than one heart-in-mouth moment.

So what’s going on? And should you be concerned?

How pensions work

First, it’s important to understand that it’s normal for the value of your pension to go up and down each day.

Its value changes because, unlike the money sitting in your bank account, your pension contains lots of individual investments. And most of these investments are typically in the form of company shares (this won’t necessarily be the case if you’re approaching retirement, and we’ll come to this shortly).

Company shares are traded on stock markets, and their value is influenced by all sorts of factors, including:

- How the company is performing

- How the local and global economy is performing

- The changing political climate

- The impact of the current global pandemic

- The rate of inflation

- Changes to interest rates

...and much more.

Typically, the more uncertain the outlook, and the faster that economic conditions change, the more company shares move up and down in value.

This is reflected by your pension balance - which shows the combined value of the investments in your pension - going up and down, sometimes quite rapidly.

At PensionBee, we display your real-time pension balance in your BeeHive. It’s likely that your previous pension provider didn’t offer this feature, so you might be seeing your balance rise and fall for the first time. And this might at first seem a little disconcerting! But you can rest assured that all pensions behave in this way as they reflect market conditions.

The risk of locking in losses

It might be tempting to switch to a different pension plan when you see your balance falter. But pensions are long-term investment products, and they’re designed to weather short-term fluctuations.

For example, in March 2020 - when the global economy suddenly faltered due to sudden lockdowns to combat the emerging pandemic - stock markets fell around the world. In the US, the biggest stock market (the S&P 500) fell around 3_personal_allowance_rate in a month! But by August 2020 it had fully recovered, and a year later it was up a further 3_personal_allowance_rate.

Source: Google

A person who panicked when the market crashed and switched their pension to a lower-risk plan with less growth opportunity might be regretting their decision. In contrast, a person who allowed their pension to weather the storm and even made further contributions might be feeling quite pleased.

If you sell or switch your investments when the market’s down, you could miss out on any increases in value in the future if markets recover.

Pensions are long-term investments, and have historically weathered all short-term financial storms that have been thrown at them. And while no one can predict the future, it’s generally accepted by economists around the world that there’s no reason this trend won’t continue in the long-term.

What if you’re approaching retirement?

If you’re approaching retirement, you might be thinking, “This is all very well, but I’m retiring in a few years. I don’t have time to wait for my pension to catch up!”

You’d be right to be concerned - you don’t want your pension to lose value just as you’re about to retire.

But if you’re a PensionBee customer, you should be invested in an appropriate plan for your age, that’s less exposed to the stock market. So your pension balance shouldn’t rise and fall to the same extent as our plans designed for people further from retirement.

For example, following the March 2020 crash caused by the pandemic, where the UK stock market dropped by 24% and the US stock market by _basic_rate, our Tailored Plan for those retiring between 2025-27 fell in value by 1_personal_allowance_rate. In contrast, the Tailored Plan for customers retiring between 2037-39 fell in value by 16%. In the years since, both plans recovered and grew beyond their March 2020 losses.

It’s impossible to completely isolate your retirement savings from the wider economy - even investing in cash means you could lose value due to inflation - but being invested in a pension plan that’s designed for those approaching retirement could reduce its risk of losing value.

What happened to the markets in January?

January was a turbulent month for economies and stock markets around the world for lots of reasons.

Some of the major factors included:

- reports of rising inflation

- rising interest rates

- a weaker economic outlook

The impact of these factors mean that, in general, the cost of living and doing business is rising. And that impacts everything from the amount that people can afford to invest in their pension to the amount that businesses can afford to borrow to invest in infrastructure projects and pay their employees.

As a result, global stock markets fell in January.

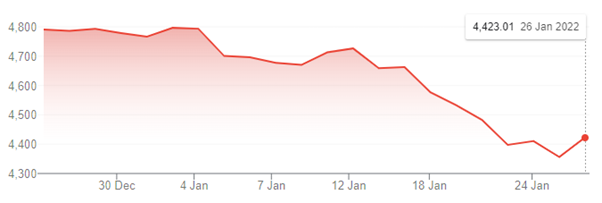

In the UK, the FTSE 250 had fallen by around 9% by 25 January.

Source: Google

In the US, the S&P 500 had fallen by around 9%.

Source: Google

In China, the SSE Composite had fallen by around 5%.

Source: Google

What happened to your pension in January?

If you’re far from retirement

If you’re invested in one of our plans designed for those not approaching retirement, your pension will likely be heavily invested in the stock market. And so you’ll likely have seen the value of your pension fall.

While no one likes to see the value of their retirement savings fall, it’s important to remember that this blip should be transitory. Historically, pensions have recovered and gone on to grow much more in the years following - just like the stock markets themselves.

Here’s another chart showing the S&P 500’s performance over the last 40 years. Notice how every fall in value was ultimately followed by an even greater rise in value.

Source: Google

If you’re approaching retirement

If you’re invested in one of our plans designed for those approaching retirement, your pension won’t be as exposed to the stock market.

Our default plan - the Tailored Plan - reduces your exposure to the stock market as you get older. For example, if you’re 65 then it will invest around 37% of your money into the stock market. Nearly all the rest is made up of fixed income investments. So you might have experienced a small drop in the value of your pension, but to a lesser extent than those further from retirement.

For more detail, you can view each of our plan’s factsheets here.

Again, it’s important to try not to fixate on short-term balance fluctuations. Short-term fluctuations are normal and expected, and even the portion of your pension that remains invested after you retire should continue to recover over the long-term.

What if you have further questions about your pension?

We understand that seeing your retirement savings go up and down can be concerning, both practically and emotionally. So we’re here to help and answer any questions you might have.

You can contact your BeeKeeper either by:

- Emailing them (find their details in your BeeHive)

- Calling 020 3457 8444 (Mon-Fri 9:30am-5pm)

You can also contact our dedicated engagement team on engagement@pensionbee.com.

Again, it’s worth remembering that it’s normal and expected for pensions to go up and down in the short-term. And it’s expected that they’ll recover and grow further in the future. But if you decide that switching to a lower risk plan is right for you, you can view our plans here.

Risk warning: As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |