Much More With Less: What I learnt from my spending diary after lockdown

As lockdown loosens, so has my spending!

I kept a spending diary during the first month of lockdown, and then again for the month from June 15 as lockdown loosened, and boy there’s a big difference. As a personal finance journalist and money blogger, I’m a fan of spending diaries as a tool for seizing control of your cash.

Over on my blog, Much More With Less, I spilled the beans on how spending for our family of four changed when coronavirus kept us cooped up at home. It’s been fascinating to see how our spending changed all over again once things started to re-open.

It’s also been fascinating to see how another family coped financially, by comparing spending diaries with fellow blogger and mum of three Lynn Beattie over at Mrs Mummypenny. (Check out Lynn’s posts during lockdown and after lockdown).

Like me, Lynn is self-employed, and lives in a four-bed house outside London - I’m in Suffolk, Lynn in Hertfordshire. Lynn is recently single but our kids are similar ages: my two are 12 (Isabel) and 10 (George) while Lynn has 12-year-old Dylan, 10-year-old Josh and Jack, aged 7.

Read on to find out where I saved, where I blew my budget, how it stacked up with Mrs Mummypenny - and what I’ve learnt since lockdown.

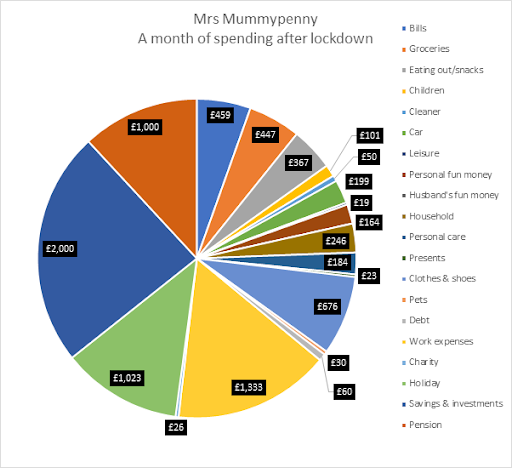

Overall

My spending definitely reflects the changes in lockdown, shooting up almost 85% compared to the first month in quarantine. Suddenly, whole categories of spending have reappeared: holidays, eating out, car costs and personal care as, for example, hairdressers re-opened.

As a result, my spending rocketed from £2,360 for the month after March 21 to nearly £4,365 in the month after June 15.

Meanwhile Mrs Mummypenny cut right back when lockdown started, limbo-ing lower than £1,800 for the month. But more recently, Lynn’s outgoings soared to £8,400 in the month since lockdown loosened - nearly double mine!

However, Mrs Mummypenny’s headline figure wasn’t all spending. Lynn actually stashed away far more cash than I did, pouring _basic_rate_personal_savings_allowance each into fixed-term savings, stocks and shares individual savings account (ISA) and pension, and investing a chunk of nearly £1,333 in her business.

Strip out those savings, investments, pensions and work expenses, and our monthly spending comes down to a virtually identical £4,144 for me and £4,074 for Mrs Mummypenny.

Within those totals, we have taken different approaches. Lynn has got right back out there, spending much more than I did on eating out, new clothes and new beds and bedding.

My big splurge was on holidays, now we can finally get away, and I forked out for the annual insurance policy for our two cars. The pandemic has also affected many people’s mental health, and we’ve spent money on counselling - something we’re incredibly lucky we can afford, faced with lengthy NHS waiting times.

Otherwise, I’m still taking a more cautious approach to our family finances, concerned about the continuing impact of coronavirus. Here’s where we spent and saved on different categories.

Bills

Bills and groceries are still two of my top five biggest spending categories, although my bills were lower than in the first month of lockdown, at nearly £590 compared to £906, because we didn’t have to fill the oil tank again. I finally caved in during lockdown, and signed up for Netflix, which adds £5.99 a month to our total. Our monthly payments for electricity went up, reflecting increased use with all four of us at home all the time. Next month, this will be lower as a friend switched to Bulb using my referral link, so we both get £50 credits.

We also had to pay our annual bill to the council, for emptying the garden waste wheelie bin.

Mrs Mummypenny’s bills were lower, while she’s taking advantage of a mortgage repayment holiday. Thankfully, we cleared our mortgage by moving from London to Suffolk, and don’t have any debt payments.

Groceries

I hoped to see my groceries bill fall after lockdown, but that hasn’t really materialised.

As I started going back to supermarkets, rather than relying on deliveries, I was able to start buying some cut-price short-dated food again, and also picked up a £3.09 Too Good To Go box from Morrisons.

However, starting Plastic Free July, and trying to buy food locally without plastic wrapping, has kept my food spending not far off lockdown levels: £456 compared to £478, so only 5% lower. Lynn’s grocery bill was almost identical, at £447 in the month after lockdown.

Eating out

Eating out has returned after lockdown, for the bacon sandwiches and ice cream when we were first allowed to drive to destinations further afield and headed to the beach at Walberswick. We also treated ourselves to a rare takeaway from a local Indian restaurant. £68.60 well spent.

Meanwhile Mrs Mummypenny has been delighted at the chance to grab drinks and eat out again, racking up nearly £337 including a Chinese takeaway, several lunches at Café Vero, Subway, Wagamamas, a pub and a celebratory meal out in London.

Holidays

Holidays surged from zero during lockdown to more than a third of our monthly spending - far and away our biggest spending category at a chunky £1,520. Spot the peak prices during school summer holidays!

As holiday accommodation re-opened, we booked a week in a holiday cottage on a farm in Yorkshire, with access to a shared swimming pool. We also picked up a last-minute vacancy on a gorgeous glamping site locally.

The nearest I got to a saving was using Snaptrip.com to search for a holiday cottage, with a best price guarantee and the chance to earn £45 cashback from TopCashback on the booking. After months and months of being stuck at home it feels amazing to stay somewhere else overnight.

Mrs Mummypenny also spent just over _basic_rate_personal_savings_allowance on holidays, for a week in Norfolk, train to Penzance and a hotel there, plus a flight to the Scilly isles and deposit on accommodation.

Car

After spending zip all on cars during lockdown, the annual car insurance bill for our two cars, plus finally needing petrol, pushed this category over £370. At least the premium was lower than last year, with a longer no-claims bonus now we’ve owned our hybrid second car for over a year.

Lynn spent pretty much the same during lockdown as afterwards – £186 versus £199 – with her regular monthly payments for car financing and insurance.

Personal care

Personal care came from nowhere during lockdown to become my third highest spending category. My husband and I were delighted to get to the hairdressers, after they reopened, and my husband also had a physiotherapy appointment for back problems working at our dining table. The impact of lockdown also showed in the cost of counselling, pushing the total up to just under £550 for the month. Tough times.

Lynn also paid for counselling in the aftermath of her divorce, taking her personal care category to a little over £184.

Leisure and fun money

Our spending on leisure and fun fell since lockdown, from nearly £265 to just over £200, perhaps because once we could go further afield, I made fewer guilt-driven purchases trying to keep the kids entertained.

My own ‘fun money’ went on flute lessons and WeightWatchers membership, plus a novel and a china plate on my first visit to a charity shop since lockdown, while my husband’s fun money went on bass guitar lessons and subscriptions to Apple music and the Guardian.

On the leisure side, with cinemas still closed, I spent a few pounds on DVDs during my trip to the charity shop, and we downloaded a couple of films onto a tablet before heading to the glamping site.

We also booked timed tickets to Ickworth, the National Trust site where we met a friend for a picnic for her birthday. Wonderful to be able to meet up with people outside our family once again!

Mrs Mummypenny’s spending on leisure and her personal fun money went from just under £180 to £164, including getting her nails done, as salons reopened, hair dye and supporting local businesses with a Standon calling poster.

Children

Expenses for my children mainly went on my son’s piano lessons by Zoom, and weekly work packs preparing for 11+ exams for secondary school. I also got my daughter a new top.

Otherwise neither of my children returned to school before the end of the summer term, so I’m holding off buying new school shoes and uniform until just before term restarts in September, in case they grow even more.

Clothes and shoes

I still haven’t spent anything on clothes or shoes, but Lynn really went for it at just over £_pension_age_from_20286, including a couple of fab dresses from Retro Revival.

Cleaner

I carried on paying my cleaner during coronavirus, but it’s been a big relief now she’s able to return each week. Our home is now a distinctly nicer place to live. We spent nearly £100 over the month, while Lynn spent half as much on a couple of visits.

Household

Our household spending nudged up from £58 to £80 odd, mainly because we could finally get the boiler serviced once non-emergency appointments resumed. I also paid to get shampoo and conditioner bottles refilled, as part of Plastic Free July.

Meanwhile Mrs Mummypenny spent roughly the same £250 during and after lockdown, driven up this month by a couple of new beds and bedding.

Other categories

My spending on presents went up a little after lockdown, from nearly £50 to £78, celebrating three birthdays including my sister’s and a friend’s son’s 18th – no chance of a big 18th birthday bash! Lynn spent a bit on a present for one of her children’s teachers, tea and face masks, rising from £18 during lockdown to £23.

Otherwise, we both spent minimal amounts on pet food, and I picked up poo bags and puppy snacks when a local shop re-opened. I donated a tenner to Concern Worldwide for Syrian refugees, while I brace myself before taking the Ration Challenge again, while Lynn spent £26 on a ticket to a charity event.

Work expenses

My work expenses came down compared to lockdown, at £41 compared to £156, as I didn’t buy anything major this month: printer paper, software and newspaper subscriptions.

Otherwise I spent a little opening a Transferwise card and account, as increased blog traffic during lockdown mean I’ve been able to join an ad agency, Mediavine. Transferwise should help cut costs when transferring ad earnings paid in US dollars into pounds.

Normally I work from home in glorious peace, but it’s been tricky juggling work and home schooling with my husband and children around 24/7. Lockdown may have loosened, but my husband and kids still aren’t back in the office or at school.

Meanwhile Lynn made the most of the time her children spent with her ex and invested big time in her business, with work spending up from £254 to £1,333. This included expenses of nearly _basic_rate_personal_savings_allowance for a website redesign and photo shoot for new profile pics, plus editing costs for her new book, The Money Guide To Transform Your Life, business coaching, accounting software and subscriptions for software, Zoom and podcast hosting.

Savings, investments and pension

During lockdown I finally set up a small monthly pension payment, so that went out, plus regular transfers into an investment app I’ve been testing. These outgoings were similar during and after lockdown: £1_state_pension_age versus £180. I’m intending to top up both investments and pensions with lump-sums later in the financial year, depending on my freelance work flow.

Lockdown really focused Mrs Mummypenny’s mind on setting aside money for the future. When lockdown started, Lynn was keen to conserve cash, and only put £120 in savings. Since then, taking a three-month mortgage payment holiday freed up £3,600 that would normally go to her lender, so Lynn was able to split £3,000 equally between fixed-term savings, her stocks and shares ISA and her pension. Lynn is delighted that she’s been able to build up her emergency fund to six months of essential expenses.

Lockdown learnings

Lockdown was a great leveller. As so much shut down, spending focused on essential bills and groceries for me and Mrs Mummypenny.

Since restrictions loosened, I’ve seen my spending surge, driven by different categories of holidays, car costs and personal care. I remain keen to support small businesses where possible, such as buying food from the local butchers, fish van and Hadleigh market, birthday presents on the high street and music lessons from local teachers.

However, I’m still cautious about splashing much cash on non-essentials. I’m so grateful we had enough savings, and our finances were stable enough, to afford the holidays but we won’t be visiting many shops or restaurants.

Meanwhile Lynn has spent much more on eating out, clothes and household expenses, seized the chance to invest in her business and also set aside large sums towards her financial future.

Lockdown rules may have changed, but life hasn’t returned to normal yet, and nor has our spending. With the potential for a second wave of coronavirus, and further damage to the wider economy, I’m still keen to keep up my spending diary and keep my spending down.

Faith Archer is a Personal Finance Journalist and Money Blogger at Much More With Less. Check out Faith and Lynn’s videos about spending during lockdown and after lockdown.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |