.webp)

The Hidden Trap Costing Job Hoppers Thousands in Retirement Savings

In today’s dynamic job market, frequent career moves are common, especially among younger professionals. However, this trend has led to a growing issue: abandoned 401(k) accounts. Recent estimates indicate that over 29 million forgotten 401(k) accounts exist in the U.S.

To make matters worse, when employees leave behind small 401(k) balances - under $7,000 - employers can transfer these funds into Safe Harbor IRAs without the employee's consent to help manage high volumes of inactive accounts.

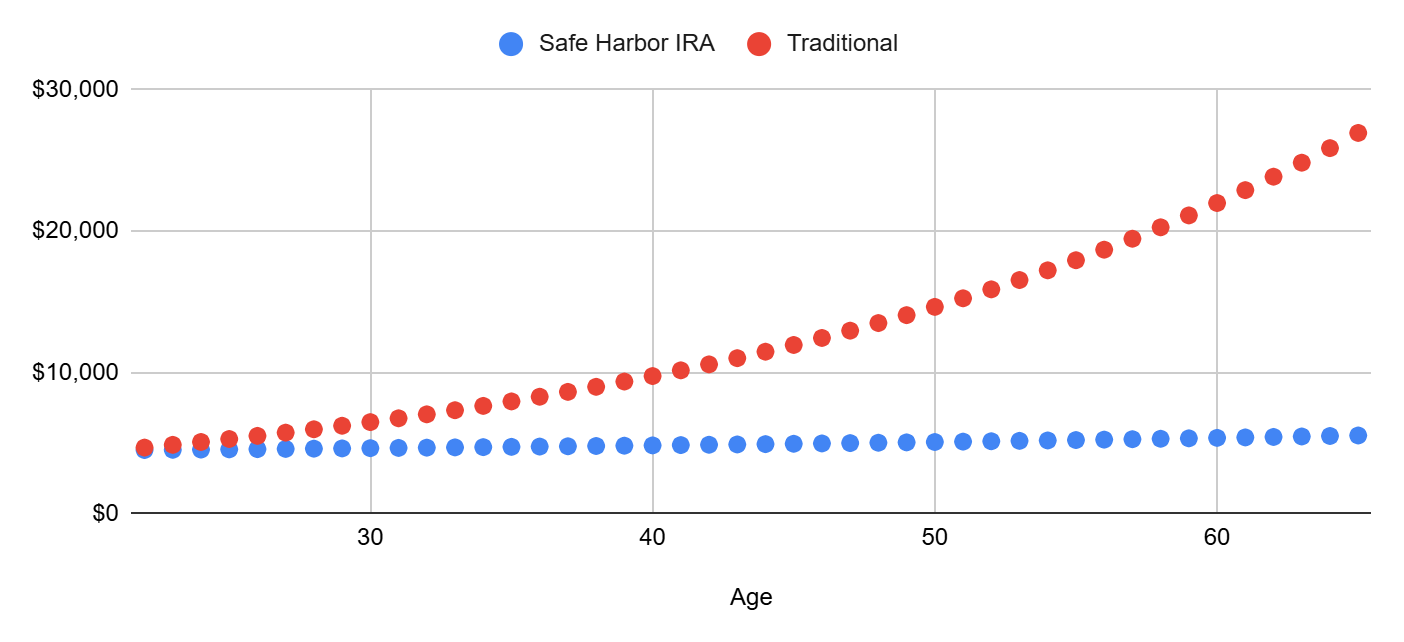

PensionBee examined the impact of this common administrative practice, revealing the stark return differential between Safe Harbor IRAs and traditional retirement accounts. Americans who leave behind just a handful of accounts early in their careers can lose out on over $90,000 by the time they retire.

The Three-Fold Problem

Safe Harbors IRAs are designed to preserve rather than grow capital. Previous market analysis by PensionBee found that combined high fees and low returns of many mainstream providers are not fit for purpose, and may even deplete forgotten retirement accounts to $0.

The problem is threefold:

First, mandated ultra-conservative investments. Regulations require Safe Harbor IRAs to use low-risk investments, usually offering far below standard retirement portfolio returns, often below the rate of inflation. Many Safe Harbor IRA providers use bank deposits with very low interest rates, sometimes as low as 0.5%.

Second, many providers charge excessive fees that devour returns. Unlike 401(k) plans, which have an average fee of approximately 0.85%, Safe Harbor IRAs charge seemingly small monthly fees ($1-$5) that quickly accumulate. One provider charges $5.67 monthly plus 0.5% annually—on a $3,500 account, that's $85.54 yearly (2.4%) before additional withdrawal fees of $75 per transaction. These fees often exceed any earnings and actively deplete principal.

Third, interest skimming. Certain providers have been known to pay less than 1% interest while prevailing rates exceed 4%, taking substantial portions of investment returns as a “bank servicing fee.”